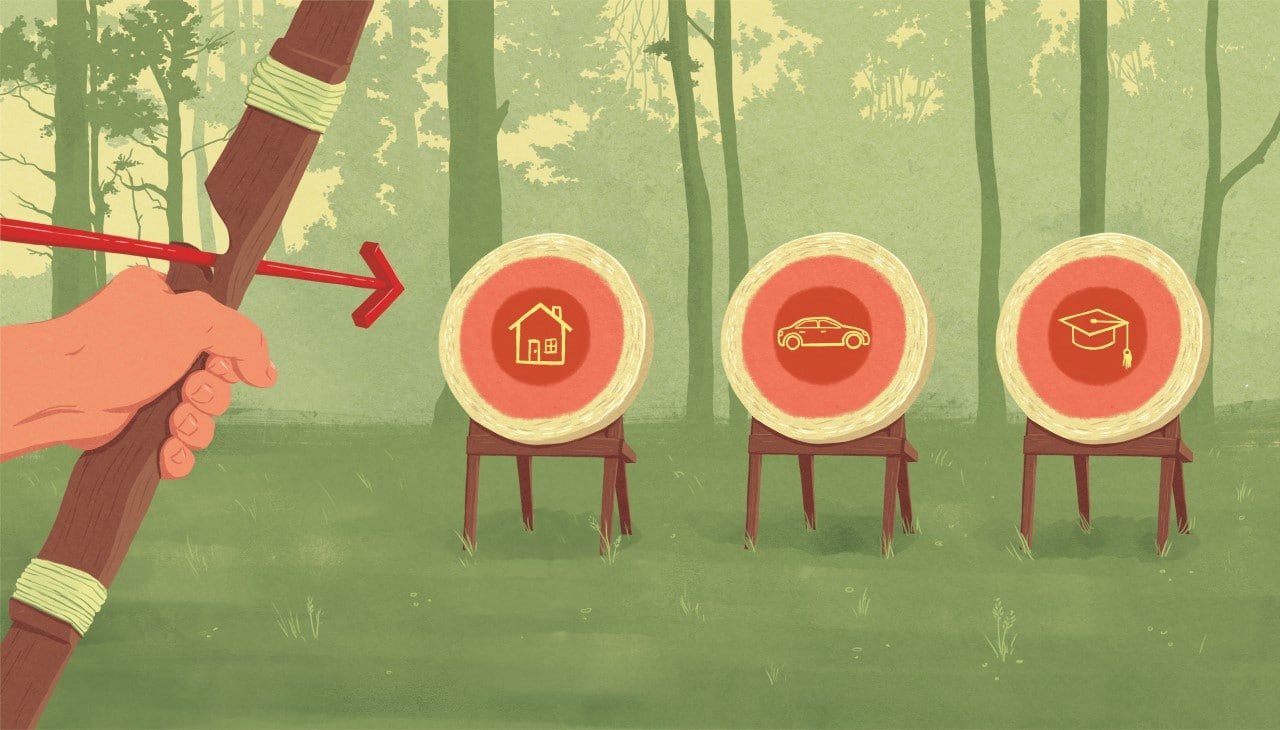

Goal-based investing: Take aim with your savings

Goal-based investing and saving can be a catalyst to build new money habits. Here's why it works and why it may be something for you to think about.

Imagine a soccer game without a goalie’s net or an Olympic race without a finish line. How about a working week without a weekend?

These examples may seem ridiculous, but there is a common denominator: Without a goal in mind, the point of some activities just seems to disappear. And our motivation to accomplish our tasks likewise just vanishes.

Here’s one more example: Imagine saving a certain amount of money for something important without deciding exactly what it is, without setting a financial goal or even establishing a timeline.

If that sounds counterproductive, well, it is. And that, in a nutshell, may be why some people have difficulty with saving and investing. We often fail to set clear goals for our money, or if we do, they may be fuzzy or unrealistic. Simply put, we may not be setting ourselves up to achieve the milestones that are important to us.

It’s not that we’re unsophisticated. We know we’re supposed to be smart with our money but taking the steps to save for a future financial goal, whether it’s a nice vacation or paying for a wedding, can be daunting at the best of times. At the worst, we may be faced with numerous other distractions and financial obstacles.

The good news is that introducing “purposeful action” into your life (and your finances) can bring benefits and advantages. The subject of goal setting has been studied by psychologists for nearly a century, and it is now accepted that if you have a clearly defined goal, you’re more likely to achieve it.[1]

The process of goal setting also has applications in our personal lives (acquiring good habits, kicking bad ones), as well as in work settings with the established conclusion that setting specific goals increases performance.[2]

When it comes to saving and investing, research suggests that if you assign realistic and tangible goals to your financial activities as well, you’re more likely to accomplish what you want.[3]

Here are some ways financial goals may be able to make you a more successful saver and investor.

Goals can provide focus

We all know we should save money for our future, but many of us are unsure of what it is exactly we are saving for or when we might need that money. For example, some people hope to one day take that vacation they’ve been dreaming about all their lives — say, a family trip to Florida. Unless we take specific action to prepare financially, this kind of dream vacation may remain wishful thinking. Don’t feel bad if you are prone to this kind of procrastination: Putting off concerns that are far in the future is something humans do by default. We tend to deal first with obligations that need immediate attention.

But if you set measurable and defined goals, your focus may become clearer. A family vacation to the sunny south can be broken down into individual expenses and decisions, including flights, accommodations, restaurants and activities. You can give yourself a deadline on when you want to go — let’s say five summers from now — and you can begin to save and invest towards accomplishing this financial goal. Using a Tax-Free Savings Account (TFSA) could help your savings grow towards your travel goal. Start by asking yourself just how much money you need to put away to ensure that when the time comes everyone is enjoying themselves on the beach.

Goals can help us make better decisions

Let’s take a typical homeowner who is faced with the costs of maintaining a home: She would like to renovate the kitchen and basement and buy a new washer and dryer, but she’s also mindful that she’ll need a new roof soon. With a limited budget, the homeowner must decide which goal takes priority.

She decides that living under an old roof could damage the home, so fixing it is a priority. While her kitchen and basement renovations might be the most gratifying (she’s already picked out designs and paint), these are optional. The unknowns are the appliances: The household can’t function without them, but they might last a while, or can be repaired rather than replaced.

This example demonstrates that not all goals are created equal. They each have different costs (of course), but also different timelines, levels of priority and even emotional attachments. The same analysis of goals can be used for your finances. Buying limited edition sneakers may bring immediate enjoyment, but you might also want to ask yourself, “Could I have put this money towards owning a home?”

For those whose goal is home ownership, a First Home Savings Account (FHSA) is designed to help you save for your first home, tax-free and may help you reach your vision of owning a home faster.

Goals can be motivators

Goals can also push you into action. Here’s an example: Many parents hope to help their children pay for post-secondary education. The cost of schooling (and student accommodation) is expensive and climbing, and that means you may require a dedicated savings plan to meet this need. If you have a young child who you hope will attend university, college or trade school one day, you may be highly motivated to open a Registered Education Savings Plan (RESP), which can boost your savings through government grants.

The goals that motivate you are often personal. It might be putting aside some savings to take care of holiday bills, or it could be something bigger like saving to retire earlier. If you are unclear what your money can do for you, you may want to speak to a TD Personal Banker who can suggest what needs you should map out for the coming years. For example, if retirement is on the horizon, a Registered Retirement Savings Plan (RRSP) not only has tax benefits but can also allow your savings to grow over the long term to help finance your retirement.

Goals can measure your progress

The famous quote, “you can’t manage what you don’t measure,” applies here. Measuring your progress in any endeavor can help ensure you’re on track. For example, if you are trying to shape up and have a goal to lose 15 pounds, you could divide the task up into monthly and weekly goals to measure your progress. You may even see the relationship between your efforts and the short-term result and re-adjust your efforts accordingly — more exercise? More salads?

This can work for financial goals too, like paying off student loans or saving for when a child is on the way. You can divide your overall objective into increments and see how you progress weekly, monthly or annually. You may even want to put your savings into a separate account to more clearly observe your progress. Alternatively, you can also have a TD Goal Builder conversation with a TD Personal Banker at your branch to define your financial goals and track your progress towards them online.

Measurement is a great motivator: Seeing how much you are accumulating may nudge you to find additional ways to save more, invest more efficiently and perhaps even come up with a bigger goal for your money.

DON SUTTON

MONEYTALK LIFE

ILLUSTRATION VERONICA PARK

Book an appointment with a TD Personal Banker

[+]

| ↑1 | Latham, G. P., The motivational benefits of goal-setting, Academy of Management, Vol. 18, No. 4, Decision-Making and Firm Success (Nov., 2004), pp. 126-129, accessed dec. 14, 2023, www-2.rotman.utoronto.ca/facbios/file/15%20-%20Latham%20AME%202004.pdf |

|---|---|

| ↑2 | Locke, E. A., and Latham, G. P. (2002). Building a practically useful theory of goal setting and task motivation: a 35-year odyssey. Am. Psychol. 57, 705–717. doi: 10.1037/0003-066X.57.9.705 |

| ↑3 | Blanchett, David, “The Value of Goals-Based Financial Planning.” Journal of Financial Planning, 2015, 28 (6): 42–50. |

DISCLAIMER: The information contained herein is for information purposes only. The information has been drawn from sources believed to be reliable. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the fund facts and prospectus, which contain detailed investment information, before investing. Mutual funds are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer and are not guaranteed or insured. Their values change frequently. There can be no assurances that a money market fund will be able to maintain its net asset value per unit at a constant amount or that the full amount of your investment will be returned to you. Past performance may not be repeated. Mutual fund strategies and current holdings are subject to change.

TD Mutual Funds and the TD Managed Assets Program portfolios are managed by TD Asset Management Inc., a wholly-owned subsidiary of The Toronto-Dominion Bank and are available through authorized dealers.

Mutual Funds Representatives with TD Investment Services Inc. distribute mutual funds at TD Canada Trust.

® The TD logo and other trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.